AIM13 Commentary - 2016 Q4

“The greatest trick the devil ever pulled was convincing the world he didn't exist.”

- Kevin Spacey as Roger “Verbal” Kint, The Usual Suspects (1995)

February 24, 2017

Dear Investor,

If the primary basis of your belief that something will happen in the future is that it has always happened in the past, at what point do you abandon that belief when an almost unprecedented amount of time passes without it happening? We do not often start our letters with such heady questions, but after eight calendar years of positive gains in the U.S. equity markets (as represented by the S&P 500 Total Return index (the “S&P 500 TR”)), we know many people are abandoning hedged investing – or at least strongly bemoaning the returns relative to long only equity. However, even as the Dow sails past 20,000 and the S&P 500 is at an all-time high, we continue to believe that significant market corrections happen and that bear markets exist. While we may sometimes sound like a broken record, we will not be “tricked” into believing otherwise. Our thoughts on why we are not changing our investment philosophy are below.

It is important to understand the election’s impact on the market return for the year. For the first ten-plus months, through Friday, November 4th, the S&P 500 TR had gained 3.88%. In fact, right before the election, the S&P 500 TR slid nine days in a row – its longest string of losses in 36 years! Then in the last 38 trading days (which is only about 15% of the total trading days for the year), the market surged, in that short period contributing roughly 65% of its calendar year return.

Although hedge fund investors generally were not happy to trail the S&P 500 TR by the wide margin we experienced in 2016, the type of upward move inflection caused by Donald Trump’s surprise election (or some other mini-black swan type of event) will almost always cause hedge funds to lag. However, does this mean we abandon the strategy?

We cannot predict the future, and we have not abandoned hedged investing with talented active managers for the majority of our portfolio. Yes, the U.S. equity markets continue to climb higher. Indeed, just recently the S&P 500 market cap reached a record $20 trillion. (Putting that in perspective, four years ago, on January 1, 2013, the total market cap was $13.5 trillion.) However, even if we had been told on March 9, 2009 that we were on the verge of such an almost unprecedented bull run, we still would not have put all of our money in an equity index fund.

“Mea culpa, mea culpa...”

One could say we were wrong not to put our money allocated to the public equity markets in inexpensive index funds back in 2009. Indeed, investors who chose to do so are now held up as geniuses. For instance, the New York Times ran an article recently lauding the investment prowess of Houghton College, an upstate New York college with an endowment of $46.4 million, because its endowment return bested the likes of Harvard, Yale, and other large endowments last year by a wide margin. How? According to the Times, “Houghton got out of hedge funds and all alternative investments a year and a half ago, and moved the entire portfolio to a mix of low-cost index funds and mutual funds at the fund giant Vanguard.” As we have noted before, that is a common solution for those who have given up on hedge funds. We would caution Houghton College, however, that the S&P 500 is in its 96th month of a bull market. This represents the second-longest bull market since 1926:

Source: J.P. Morgan Asset Management

With such a long period without a significant pullback, does that mean that pullbacks won’t happen in the future? Or that bear markets do not exist? Of course not. As a reminder, consider the recent history of intra-year declines in the S&P 500 represented below:

This chart is particularly interesting for a number of reasons:

- In the past 37 years, the average intra-year drop has been -14.2%. Yet in the last five years (2012-2016), we haven’t seen a decline of greater than 12%, and the average pullback in that period has only been -9.2%. Compare that to the prior five year period (2007-2011). In that period, four of the five years had greater than average declines, and the average pullback was -24.4%.

- There are also trends in the magnitude of the declines year over year that could be a leading indicator of the pullbacks that follow. For instance, in the years 1995-1998, each year saw ever increasing intra-year declines, and subsequently the market experienced a true correction in 2000-2002. The same trend occurred in 2005-2007 prior to the financial crisis in 2008. When we look at 2013-2015, we may have seen a similar pattern, year over year of increasingly greater intra-year pullbacks.

- About one-third of the declines in the prior 37 years have been greater than the average of 14.2%. The question is when we have such a pullback, will long only investors stomach the loss? Put differently, will the Houghton Colleges of the world allow as much as a quarter or more of their endowments to disappear without moving to cash and protecting what remains? Such would be a classic case of buying high and selling low.

Being “wrong” about remaining hedged in a rising market has its silver lining. In the past five years, when hedge funds generally have lagged the broader equity markets, by many measures the economy has done well, which is a good thing for everyone overall. Certainly, the S&P 500 TR has surged, producing annual returns of 14.7%. Unemployment went from over 8% to under 5%. The budget deficit came down, inflation has been kept below average, and housing prices have been rising. What this means is that while our hedged investments may have lagged the S&P 500 TR, other allocations (private equity, real estate, etc.) have benefited from a relatively supportive environment.

We realize that in order to look “good” relative to equity market indices such as the S&P 500 TR, we should be rooting for a serious market correction. Frankly, we are rooting for precisely the opposite. Indeed, over the last ten years (through December 31, 2016), the S&P 500 TR gained only 6.9% annually, well below its nominal average return since 1900 of about 11.5%. Our preference is for the market to out-perform its historical average. Unfortunately, not only can it under-perform, but the market can even produce zero price returns for extended periods of time, as it has two times in the last fifty years:

Extended Periods of Zero Percent Price Change

in the S&P 500

While we are not rooting for a serious correction or long periods of zero returns, we remain prepared in case these things happen. In that regard, in the spirit of being aware of the more obscure patterns in the markets, we came across an interesting chart that indicates that the worst year of any decade for the Dow has been the seventh year – or the year we currently face, 2017:

The Ten-Year Stock Market Cycle:

Annual % Change in the Dow Jones Industrial Average

Source: Real Investment Advice

Due Diligence Tips

We are finding more and more that managers sometimes need to be reminded of their legal obligations to their partners. For instance, all managers registered with the SEC must provide clients with a copy of their internal Code of Ethics. Some managers balk at this since the Code of Ethics includes the manager’s personal securities trading policies, or the rules that govern an employee’s trading in his or her individual accounts. Either feigning ignorance of the rule or relying on the technicality that the manager’s “clients” are the funds they manage (not the partners in the funds), some managers resist handing over the Code of Ethics. We always insist on reviewing the Code of Ethics, since how managers and their employees personally invest their own capital is a good indicator of how they think about the markets and their partners, especially if it deviates from the mandate of the manager’s fund.

We also continue to press managers on expense practices and, in particular, have been spending a lot of time analyzing trading costs. We have always known that trading practices among our current managers and new managers we consider for the portfolio can vary widely. However, with greater transparency and improvements in market efficiency and technology, our managers are finding more opportunities to reduce costs, improve execution quality, and generate better returns. Leveraging our ability to cross-pollinize good ideas, we are analyzing each manager’s trading costs per share and as a percentage of fund assets, use of soft dollar credits and how those credits are allocated among manager vehicles, and commission sharing agreements. This is a rapidly evolving area of investment management, especially with the implementation of MiFID II in Europe, which increases the transparency of trading costs relative to research-related services provided by brokers.

Our final tip is one useful for reading footnotes (which we do a lot of): Not many people know that Apple included a magnifying glass function among its camera modes in the latest version of its software. Called the "Magnifier," the new setting is found in Settings > General > Accessibility. Just turn "Magnifier" on. Then simply press the home button three times anywhere on the device – either on the lock screen, the home screen, or in an app. Now you are ready to read the fine print!

Market Observations

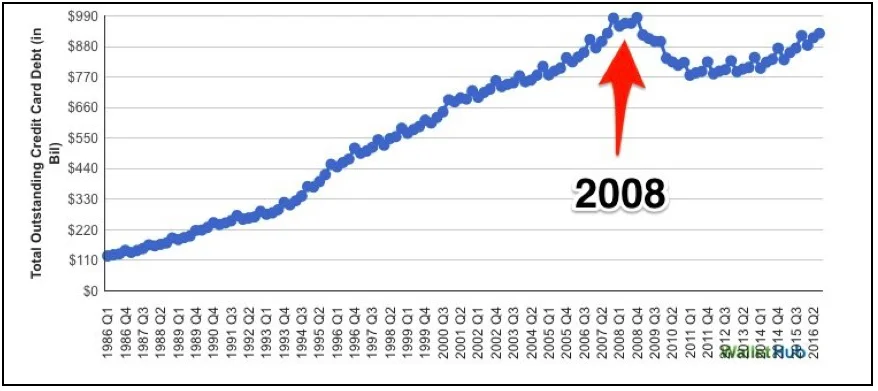

- The over-burdened consumer. JP Morgan reported late last year that six million Americans have stopped paying their car loans (as measured by being more than 90 days late on payments). In fact, the subprime delinquency rate slipped to 2% last year; the only other time it was 2% or more was following the financial crisis, according to research published on the New York Fed’s Liberty Street Economics site. The chart below reinforces the troubling trend for the consumer:

Total Outstanding Credit Card Debt Q1 1986 - Q3 2016

Source: Business Insider

What is most disconcerting is that ballooning consumer debt is not just a problem in the U.S. The chart below shows the trend in Canada, where the total consumer debt recently crossed the two trillion Canadian dollar level for the first time, according to a Bank of Canada report released in January.

Canadian Consumer Debt

Source: Bank of Canada

Where this consumer debt bubble will lead is anyone’s guess, though past debt bubbles have not ended well. One thing we do know is apparently where these consumers are shopping: According to research published by ValueWalk in early January, Amazon is now worth more than Macy’s, Kohl’s, Sears, JC Penny, Nordstrom, Best Buy, Barnes & Noble, Dillard’s, Gap, and Target – combined.

- Gold and the VIX. The low levels of volatility in the market normally is a sign of a lower risk environment. However, as James Mackintosh of the Wall Street Journal recently pointed out, “The last time U.S. stock market volatility started the year this low was in 2007, shortly before the subprime crisis hit.” Likewise, there has been a noticeable uptick in flows to gold. RBC noted earlier this month that “we have seen an acceleration of inflows into physical gold ETFs” which in turn has driven up the price of gold.

Price of Gold

- Selling by insiders of financial stocks. The surge in the financial sector following President Trump’s election is not surprising given his campaign promise to reduce financial regulation, lower taxes, and promote pro-growth economic policies. (No surprise that Goldman Sachs stock recently hit at an all-time high.) What was less reported was the selling by those company’s corporate insiders. In fact, the Wall Street Journal reported on January 24th that company leaders at J.P. Morgan, Morgan Stanley, and Goldman Sachs sold nearly $100 million in stocks since November 9th – the most in that same period in any year over the past decade.

We will end this section by noting that on February 6th, Bloomberg released the following graph that tracks usage of the word “uncertainty” in media stories:

A Note About the DOL’s New Fiduciary Rule

There has some press regarding President Trump’s anticipated effort to stop the implementation of a new rule from the Department of Labor to impose fiduciary standards on all finance professionals who work with retirement plans or provide such plans and retirees investment services. The rule, known as the DOL Fiduciary Rule, announced last year caused a stir because, among other things, it mandated that advisors clearly disclose fees and commissions, reveal any conflicts of interest, and otherwise act in the “best interest” of clients. Brokers and other service providers fought the rule, since under the previous rule of only “suitability,” they were not held to as high of a standard of good practice.

While our bias is always against unnecessary regulation, we viewed this dust-up regarding the rule as a little puzzling. As an investment advisor, we have always been held to the higher fiduciary standard. Being told to act in the best interest of clients and not to hide fees, expenses or conflicts of interest is sort of like being told to do the right thing.

We thank you for the confidence you have placed in us and welcome any questions or thoughts you may have.

Sincerely,

Alternative Investment Management, L.L.C.