AIM13 Commentary - 2016 Q2

“Insanity is doing the same thing over and over again and expecting different results.”

- Albert Einstein

August 23, 2016

Dear Investor,

Readers of our letters will not be surprised to hear that we are deeply unsettled by the ever rising equity markets. On August 11th, the S&P 500, NASDAQ, and Dow all hit record highs on the same day, which has not happened since December 31, 1999. Investors continue to push equity levels higher, to pull money from hedge funds, and to act as if this bull market will go on forever – despite significant warning signs in the markets. In a mid-July press conference (which we guess most investors missed), ECB President Mario Draghi used the word “uncertainty” or something similar 13 times, including five times in just 30 seconds. Yet U.S. markets continue to go higher. In this letter, we ask ourselves: Why are investors’ expectations and how we see the world so far apart? Are investors expecting a result that will be different from the end of the last bull market? In other words: Are investors insane?

In our first quarter letter, we wrote extensively about the hedge fund industry and the problems we see with many hedge fund managers and their compensation structures. The letter, which many viewed as an indictment of our own industry, garnered a lot of feedback and criticism. Indeed, one publication ran a story on it entitled, “Manager Diagnoses Industry’s Woes.” While we were surprised by the news coverage (must have been a slow day!), we also were disappointed by the focus on what we said was wrong with hedge funds, ignoring how we address the issues and why we think hedged strategies are still appropriate for the majority of our portfolio in this environment. The general tone of the response, however, did not surprise us…

Unlike the investor depicted above (we think he works for one of the big pensions), we continue to believe hedge funds make sense for a very simple reason: In a rising equity market, we will accept lower relative returns because, given our expectations about future returns (in particular, future pullbacks), we are convinced remaining hedged will generate the best long term, risk-adjusted results. Unfortunately, time and again investors make the wrong decisions at the wrong times. No one can call a market top or a bottom. However, where were the market-timing experts on March 9, 2009, when markets bottomed out after the financial crisis? We just do not understand (or maybe we do…) why people continue to follow the herd, many times like lemmings over the cliff!

Our expectations about future returns, it seems, are different than most investors’, especially those who think they will be better off in long only equity funds. That observation got us thinking more generally about expectations and reality. We believe the chart below identifies the difference between the two:

Expectations and reality can widely diverge, and managing expectations to align with reality is the hardest job of any parent, coach, mentor, or, for that matter, investment manager. Expectations and reality can also be negatively skewed (or flipped on our chart above). For example, according to a survey by Franklin Templeton, 66% of investors thought the S&P 500 TR fell in 2009, no doubt associating the year with the catastrophic prior year of 2008. In fact, the S&P 500 TR gained about 26% in 2009, which is a phenomenal year by any measure. Stress, however, typically comes from expecting more from the market, and your investments, than can realistically be delivered. We see a lot of stress among today’s investors, and we have a theory about where it is coming from.

What Are People’s Current Expectations?

The truth is we are all spoiled with thirty years of largely positive equity market returns. In May, the McKinsey Global Institute published a groundbreaking report entitled, “Diminishing Returns: Why Investors May Need to Lower Their Return Expectations.” The report led with the following graphic:

Source: McKinsey Global Institute (May 2016)

Calling the period of 1985 to 2014 as “the golden era for investment returns,” McKinsey offered this sobering outlook:

“Most investors today have lived their entire working lives during this golden era, and a long period of lower returns would require painful adjustments. Individuals would need to save more for retirement, retire later, or reduce consumption during retirement, which could be a further drag on the economy. To make up for 200 basis point difference in average returns, for instance, a 30-year-old would have to work seven years longer or almost double his or her savings rate. Public and private pension funds could face increasing funding gaps and solvency risk. Endowments and insurers would also be affected. Governments, both national and local, may face rising demands for social services and income support from poorer retirees as a time when public finances are stretched.”

- McKinsey Global Institute, May 2016

This type of forecast is not out of the ordinary. Blackrock also expressed a bearish forward-looking view in its July 2016 Capital Market Assumptions report: “Our five-year return assumptions are generally lower than our long-term equilibrium projections across most asset classes due to elevated valuations and our modest economic growth expectations.” GMO’s most recent outlook is even more grim, forecasting -3.2% annual real returns for large cap stocks over the next seven years:

GMO'S 7-Year Asset Class Real Return Forecasts

Source: GMO LLC (as of July 31, 2016)

Taking this all together, it seems to us that return expectations should be lower. Unfortunately, it is not clear that investors are willing (or prepared) to adapt to this low return environment. Although flows into equity market mutual funds have slowed according to the Investment Company Institute, as noted at the outset of this letter, the stock market continues to notch new highs. According to a Goldman Sachs report in early August, since the start of the second quarter, 40% of S&P stocks have reached a five-year high and almost 60% have reached a 52-week high. When the American Association of Individual Investors published its most recent sentiment study on July 27th, it found that bearish views remain below historical averages. In fact, over 70% of respondents are either bullish or neutral on the stock market over the next six months. It seems that many people have forgotten that what goes up can also go down. J.P. Morgan reported recently that since 1980, 40% of stocks have suffered "catastrophic losses,” meaning they fell at least 70% and never recovered.

It becomes clear to us that the high market expectations of the wider investing public – which has translated into an almost unabated surge in equities over the last seven years – seem at odds with what is becoming increasingly plain to us for the future, one of much lower or even negative returns. We should note that while our overall return expectations are lower, this does not mean that there may be periods of significant positive returns, coupled undoubtedly with equally significant (or even greater) pull-backs. . For this reason, we remind investors of the power of negative numbers each quarter, by including at the end of this letter the simple math illustration of what it takes to make up losses.

What is Reality in Today’s World and Markets?

You don’t need us to tell you that we live in historically turbulent times. In the last sixty-five days alone, we have seen:

- A radicalized Islamist drives a truck through a crowd killing 84 innocent men, women, and children in Nice;

- An attempted coup in Turkey is followed by a harsh crackdown by the incumbent leader;

- Eight police officers are murdered in Dallas and Baton Rouge in two ambush-style attacks;

- The two major parties nominate candidates who both have “strongly unfavorable” ratings that far exceed any presidential candidate in the past forty years;

- The Democratic Party’s computer systems and the email accounts of almost 200 congressional Democrats are apparently hacked by the Russian government, and the subsequent release of emails leads to the resignation of the DNC chair; and

- The United Kingdom votes to end its 43-year membership in the European Union.

Leaving aside the cost in human life and suffering, which are always foremost in our minds, civil strife, domestic insecurity, political uncertainty, and global unrest are all also significant headwinds for equity market growth. Beyond these socio-political factors, when it comes to the markets and the economy itself, we see a wide array of troubling indicators:

- Corporate Earnings Recession: Earnings have been going down ever since profits peaked about a year ago. Indeed, earnings are heading for a fifth straight quarter of declines, brought down mostly by the energy sector’s struggle with low oil prices, a strong dollar, and a weak global economy. Referring to the chart below, Jesse Felder wrote recently, “Over the past half-century, we have never seen a decline in earnings of this magnitude without at least a 20% fall in stock prices, a hurdle many use to define a bear market.”

Corporate Profits Year Over Year Percentage Change

- Inventory-to-Sales Ratios are High: Inventories of cars and building materials are at their highest levels relative to sales since the financial crisis, according to research published by Zerohedge, hovering near cycle highs at 1.40x. This means of course that sales are down and inventories are up, which is not a good combination. As James Saft noted, writing in the St. Louis Post-Dispatch, “The last two times the business inventory-to-sales ratio got this high and then began to decline were in 2000 and 2008. The first time the U.S. economy was less than a year from a recession and in 2008 we were smack in the middle of one.”

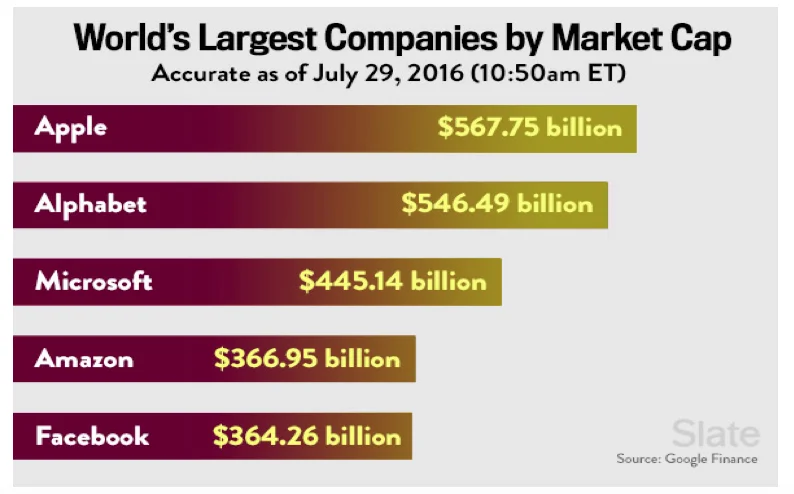

Another Tech Boom? We read recently that when Microsoft announced it was buying LinkedIn in June, it planned to pay the equivalent of $60.51 per user, a steep sum that exceeded recent per user highs for Twitter and Instagram. So it did not necessarily surprise us to see that for a time in late July the five largest companies in the world were all tech companies:

While the moment was fleeting (Exxon has since regained its place in the top five), tech analyst Patrick Moorhead from Moor Insights and Strategy pointed out: “It's really a reflection of how valuations are determined by future expectations,” he said. "It says investors are bullish on the future of tech.” Bullish or foolish?

- Declining Margin Debt: One leading indicator of stock market performance is margin debt, or the amount investors borrow to purchase stocks. As Mark Hulbert and Thomas Kee at MarketWatch have pointed out, the cash-to-margin debt ratio on the New York Stock Exchange as of late July is near an all-time low. This means that institutional investors have far fewer dollars to invest when compared to their margin debt than ever before in history.

- Consumers in Trouble: The U.S. consumer accounts for about 70% of the U.S. GDP. Unfortunately, the average consumer is increasingly burdened by expensive debt. The Wall Street Journal reported recently that credit card balances in the U.S. are on track to hit $1 trillion this year. That would come close to the all-time peak of $1.02 trillion set in July 2008:

Ten million new consumers obtained credit cards in the last year alone, pushing the total number of Americans with at least one card to over 130 million, according to a recent Industry Insights Report from credit-scoring company TransUnion.

Moreover, the labor market is not helping the situation, even as the overall jobs situation is fairly positive. According to the U.S. Bureau of Labor Statistics, since 2014, the U.S. economy has added approximately 455,000 waiters and bartenders. (This was not surprising to us when we saw Mark Perry, the AEI economist, tweet in May that, for the fourteenth straight month, and by the widest margin ever, Americans spent more at restaurants than at grocery stores.) Unfortunately, in the same period, we also lost about 10,000 manufacturing jobs, which represents a continuing troubling trend:

This growing gap between the dwindling well-paying middle class jobs (typically in the manufacturing sector) and the growth of low-paying unskilled jobs, like waiters and bartenders, is not a good trade for the American consumer or the economy.

* * *

"People do not get what they want or what they expect from the markets; they get what they deserve."

- Bill Bonner

The question becomes, why is the reality we illustrated above so far removed from many investors’ expectations about the markets? Or in other words, why has the market resumed its march higher in 2016? There are enough sources of stress in our lives. When it comes to the equity markets, we try our best to close the gap between expectations and reality. At the end of the day, as we have said many times, investing is not like Olympic gymnastics, there are no points for difficulty. It is simply about being realistic and investing with talented managers for the long term.

On one level, we are not surprised by the news almost every day of outflows from hedge funds and of large pensions reducing their hedge fund exposure. There are many hedge funds that are not truly hedged, so it is no wonder that pensions are reducing their allocations. However, as we pointed out in our last letter, not all hedge funds (and hedge fund managers) are created equal, and we will not repeat here why we have conviction in certain hedge fund managers.

The larger question is, does eliminating hedged investments make sense? Unfortunately, many in the institutional world are OK with being wrong, just not alone. When all of the so-called “smart money” runs out the door or when the trend is decidedly going one way, we think it is often best to go the other way. In other words, is now the time to eliminate a piece of your portfolio that is designed to reduce volatility with the goal of outperforming over time by protecting the downside? After a seven year bull market, have investors really learned anything from their past mistakes?

We realize we are more focused on risk and what can go wrong relative to most people. For instance, we have “go bags” for every employee in the office; we have water bobs to store water in our bath tub; and we even recently acquired a window repel system to vacate our 12th floor space the fast way. However, we still hope that buying fire insurance (or, for that matter, life insurance) will be the worst investment we ever make. Equally, we hope that having a portion of our portfolio that is hedged is the worst investment we ever make, since that would mean the market only went straight up (and we would benefit as a result from our other investments which are longer biased).

Even as we remain cognizant of the risks around us, we do see enormous opportunities for truly hedged strategies:

- As money flows out of the hedge fund space, there will be more opportunities for nimble managers to deploy capital in smaller positions that could produce outsized returns. Crowded trades have been one of the biggest headwinds for hedge fund outperformance, and reducing hedge fund assets overall will be good for hedge fund strategies, especially in long/short equity.

- We believe our focus on managers who trade individual “alpha shorts” (i.e., not using indices or other portfolio tools for hedged exposure) will pay dividends in a more normalized, valuation-based market.

- Even among managers who have lost money in recent months, the high water mark is an embedded asset. We will not stay with a manager for this reason, but it does mean that the manager works for no performance fee until our prior losses are recouped.

These are all reasons to be constructive about the net return potential in the portfolio overall going forward.

“Take good care of your future because that's where you're going to spend the rest of your life.”

- Charles F. Kettering

We know very few things about the future with 100% certainty but one thing we do know – aside from the fact that we will spend the rest of our life there – is that bull markets do not last forever. Trees do not grow to the sky, and this time is not different. We concede we are not perfect at timing the markets at the bottom and the top. (Even Ted Williams, considered one of the greatest hitters of all time, “only” batted .406 in his best year.) However, we will continue to work hard to be better at buying at the lows (by adding to managers) and at selling at the top (trimming or eliminating those we view as not the very best for the current opportunity set).

We expect the market eventually will – God forbid! – fall (and perhaps significantly), and we think that expectation is aligned with the reality we see. When it happens, we will be thankful for our hedged investments. We are not alone in being prepared for a pullback: we read recently that George Soros has doubled his short bet against the S&P 500 in the second quarter, now holding put options on about four million shares in an ETF that tracks the index. Unlike Soros, many investors look back and see only positive equity market returns and believe it will continue forever. Unfortunately, you cannot (and should not) invest by looking in the rear view mirror.

Due Diligence Tip: Liquidity

Understanding liquidity is extremely important in hedge fund investing. Unfortunately, when it comes to liquidity, we think a lot of people are burying their heads in the sand (even after pounding the table in 2008-2009 that they would never be put in this situation ever again). Many limited partners have pushed for better liquidity, which can be against their interests since many make the wrong decisions at the wrong times. Not surprisingly, however, in order to raise money, managers tend to give investors what they want. So liquidity is an ever-present risk, and we thought it would be helpful to summarize how we mitigate that risk.

When it comes to liquidity, here are some of the questions we ask managers:

- Does the investment strategy align with the liquidity terms offered to investors? We read recently of a hedge fund under SEC scrutiny that offered monthly liquidity while at the same time putting fund capital in illiquid oil and gas investments. That will not work!

- In a long/short equity fund, how liquid are the fund’s publicly traded securities? We look at daily trading volumes of individual long positions to provide some insight into the fund’s true liquidity profile and how quickly a manager could liquidate the portfolio. While there are limitations to the analysis – for instance, in stress situations, liquidity can evaporate even with widely traded securities – and we do not rely on this measure alone, it does help us understand how a manager manages liquidity. Even more telling are the liquidity trends over time

- Does the manager rely more on lock ups (initial and rolling) versus investor level gates and notice periods to manage LP liquidity? Most managers concentrate on getting long initial lock-ups, but we find that initial locks come and go quickly. In fact, we cannot remember a time when we wanted to redeem during an initial lock-up period. Rolling lock-ups (where at every 2-3 year period investors can redeem) are problematic since they periodically force investors to make an investment decision for an arbitrary period of time. Our feeling is that managers are better off managing LP liquidity risks – which can harm all investors – with investor level gates and by adjusting the notice period for redemptions. The point is that LPs need to be provided access to their capital, but managers must guard against short term liquidity rights that, if acted on simultaneously in stress situations, could impair the value of the portfolio.

- Does the manager monitor its own investors’ liquidity requirements? We spend a lot of time understanding the composition of a manager’s investor base as a part of our due diligence. Knowing who else is invested alongside us tells us a lot about what liquidity pressures the manager could face in stress situations. For instance, we break out the fund LP base by investor category (pensions, family offices, individual LPs, etc.). In addition, when it comes to funds of hedge funds, here are some additional questions we ask:

- How much of the manager’s capital is from funds of funds?

- If the manager says 20%, we ask, is that 20 funds of funds at 1% each or just one fund of funds at 20%?

- What are the withdrawal terms of those fund of funds investors, how much is under lock, etc.?

In our experience, when a manager has a large investment from funds of funds, especially when it is just one or two funds, this creates enormous liquidity risk. Funds of funds have recently faced liquidity demands or even have abruptly shut down, which creates an obvious liquidity demand on the manager’s portfolio. Ironically, even when the manager outperforms other managers in the fund of funds portfolio, the manager can face redemption pressure from the funds of funds because the manager has become an outsized position in the fund of funds portfolio.

This analysis of each of our managers’ liquidity is then rolled up into our own aggregate liquidity profile, which dictates the liquidity we can offer to our own investors. We call this our liquidity asset-liability match, and we strive to maintain a “balanced” profile – i.e., all investors’ liquidity demands could be met in a worst-case scenario if everyone who had a right to redeem requested a full redemption.

A Word on the Current Wave of Terrorism

Words cannot express the horror and sadness we experienced during the spate of terrorist attacks in June and July. As long term readers of ours know, we firmly believe that the threat of terrorism has become an immutable constant in all of our lives. Whether you live in a large city like many of us do or elsewhere, the attacks in Orlando and San Bernardino, and in small towns in France and Germany, teach us that nowhere and no one is immune. The increased pace of the attacks is truly startling: according to IntelCenter, which tracks acts of terrorism, since June 8th through early August, there had been a significant attack directed or inspired by Islamist terrorists every 84 hours in cities outside the war zones in Iraq, Syria, the Sinai, and Libya. When we factor in those strife-torn areas – where the atrocities are far greater and happen almost every day – the conclusion is inescapable that the civilized world is truly at war.

We must be vigilant and, above all, if we see something suspicious, report it immediately. In this new world, we need to be extra aware of what is going on around us. When we read that travelers at JFK Airport on August 14th who heard fans cheering Usain Bolt’s Olympic dash may have mistaken the commotion for an active shooter in the airport, we were not at all surprised. People are on high alert, as they should be. With football season approaching, we think of college tailgaters, where no one is thinking about a mass killing scenario, as especially vulnerable to attack. Restaurants, concerts, or even as we have seen in France just a gathering to watch fireworks are all obvious soft targets. The reality is the world has changed, and, as much as we do not want terrorists to “win,” similar to our approach to investing in the markets, we must adapt to this new reality.

Sincerely,

Alternative Investment Management, L.L.C.